Table of Content

The point is, there’s little standardization with credit scores when it comes to jumbo mortgages. Because of the much higher loan amounts, credit requirements, as well as all other guidelines, are more strict than they are other loan types. There are different mortgage types and each has its own credit score requirements. Your credit score will affect not only loan approval, but also the interest rate you’ll pay on your mortgage. If your credit scores are below your lender’s standards, it’s possible that your first mortgage application won’t be approved but, don’t give up right away.

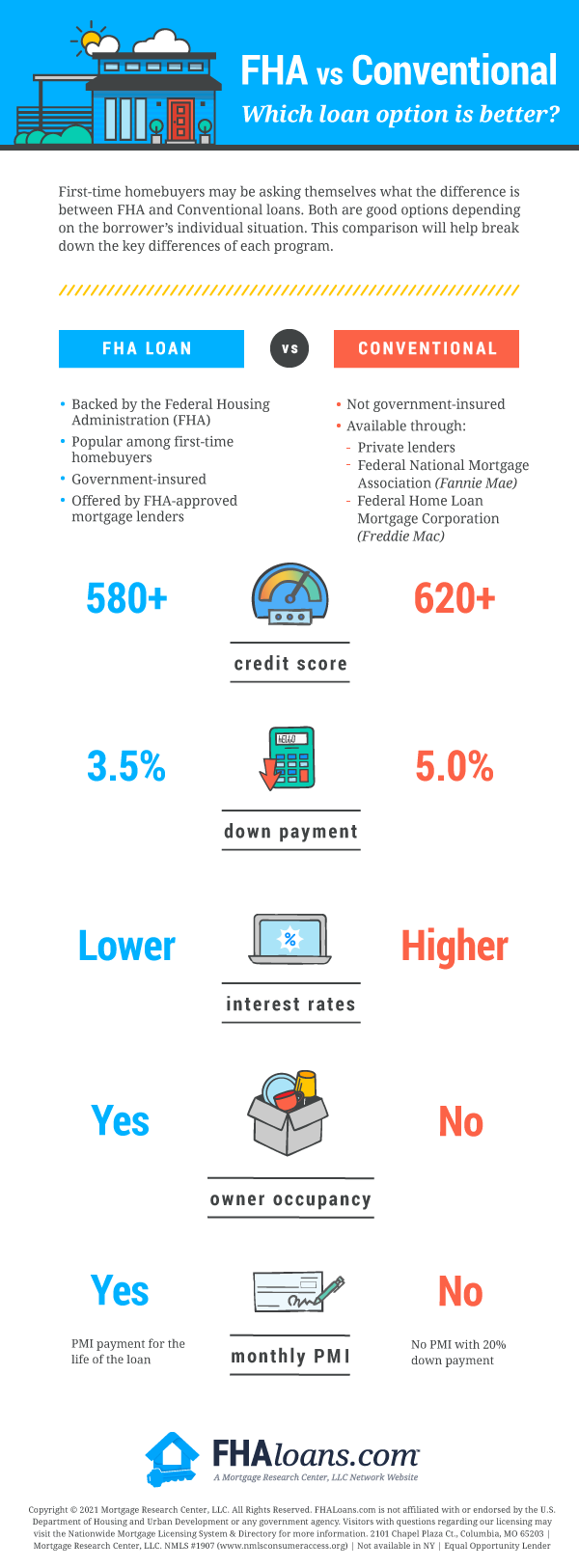

It’s recommended you have a credit score of 620 or higher when you apply for a conventional loan. If your score is below 620, lenders either won’t be able to approve your loan or may be required to offer you a higher interest rate, which can result in higher monthly payments. But what may be even more relevant when it comes to credit scores and conventional mortgages is the impact your credit score will have on the interest rate you’ll pay on your loan. Conventional mortgages are loans that are ultimately purchased by Fannie Mae and Freddie Mac, who also set the parameters for the program. They’re considered to be conventional because, unlike FHA and VA mortgages, they use private mortgage insurance companies instead of government agencies to insure the loans against default.

Do you know your Credit Score?

If your score is in the 500s, then you can actually qualify for a government-backed loan. These loans are designed to be backed by a government body, giving lenders the guarantee they need to lend to you without risk. If you have a lower credit score though, that doesn’t mean that you can’t get a loan.

The nature of the VA-backed loan is that if the holder of the loan defaults, the VA will repay a portion of the loan back to the lender. What this means in practical terms is that if you obtain a VA-backed loan but end up unable to pay, the VA will step in and pay back part of your loan to the lender. Knowing the federal government is backing at least a portion of the loan, many lenders can use this backing to work around the normal credit restrictions that limit most loans. Once you know your own credit scores, you’ll have a good idea of whether you’ll be approved for a mortgage. However, while a minimum credit score of 660 probably means you’ll get approved for a loan, you won’t get the best rates or terms. For instance, you may have to pay a higher interest rate than someone with better credit .

Mortgage Checklist: Ultimate Guide For First Time Homebuyers

Instead, it’s a standard FHA loan that provides more credit flexibility with a larger down payment. FHA will accept a credit score as low as 500 with a minimum down payment of 10%. The larger down payment makes the loan less risky, and therefore less likely to go into default. That doesn’t guarantee all lenders will accept a credit score as low as 580 on all loans.

Loans Canada and its partners will never ask you for an upfront fee, deposit or insurance payments on a loan. Loans Canada is not a mortgage broker and does not arrange mortgage loans or any other type of financial service. That’s why it’s best to consider taking the time to improve your credit score before applying for a mortgage. That way you’ll have an easier time getting approved for a home loan and clinch a lower rate, which will make your mortgage less expensive. Similarly, the loan amount required and the amortization period requested will also play a role in the credit score required for mortgage approval.

What’s the minimum credit score I need to buy a house?

As such, if your score hovers around the minimum range, you may want to make an effort to boost your score before you start house hunting. Read on to learn more about what the cutoff number means for your home-buying prospects, and how to raise your credit score if necessary. Redit score is just one element that goes into a lender’s approval of your mortgage. Money Under 30 compares the best tools for tracking your credit report and score.

To learn more about the subject, we reviewed data and reports provided by ICE Mortgage Technology. This is a software company that serves the mortgage industry. Their software programs are used to process many of the home loans that are originated in the U.S. each year. If your credit score is as low as 500, you may still qualify for an FHA loan with a down payment of 10%. An FHA loan can help trim your down payment on the purchase of a new home to as low as 3.5%, but only if your credit score is at least 580.

FHA Loans

Although we provide information on the products offered by a wide range of issuers, we don't cover every available product or service. Remember, a low score may limit your options, but it doesn't necessarily close the door on your homeownership ambitions. Even with a less-than-perfect credit history, there may still be home loan options available to you.

Your income also can’t be more than 115% of the area’s median household income. Are insured by the Federal Housing Administration, making them less risky for lenders and, because of this, easier to qualify for than conventional mortgages. Ooba Home Loans is South Africa’s largest home loan comparison service. We have a good relationship with all the big banks in South Africa, and we specialise in helping people submit their home loan applications to multiple lenders. You’ll be able to work on your credit score, making yourself more valuable as a borrower to lenders out there.

Redit score is a very important consideration when you’re buying a house, because it shows your history of how you’ve handled debt. And having a good credit score to buy a house makes the entire process easier and more affordable – the higher your credit score, the lower mortgage interest rate you’ll qualify for. In order to qualify for a home loan, you will need a minimum credit score of 580 on the FICO® scale.

Presents you with a comprehensive credit report and financial history to assess your current financial situation and credit score. You also could add a co-signer with strong credit to your mortgage application, which will improve your chances of getting approved. Just remember that co-signers assume legal responsibility for the loan if you fail to repay it. That means if you have trouble making your payments, your co-signer will be legally obligated to pay the loan. Nonconforming loans cannot be sold to Fannie or Freddie, and the minimum required credit score is up to the individuallender.

No comments:

Post a Comment